If your home experiences water damage, you have the right to a fair adjustment on a claim, and insurance companies are obligated to compensate you for your losses. However, it’s important to understand which events qualify as water damage under homeowners insurance policies and the important steps you should take to defend your claim.

A public adjuster works for you and can help with the entire claims process to ensure you get the payout you deserve from your water damage insurance claim.

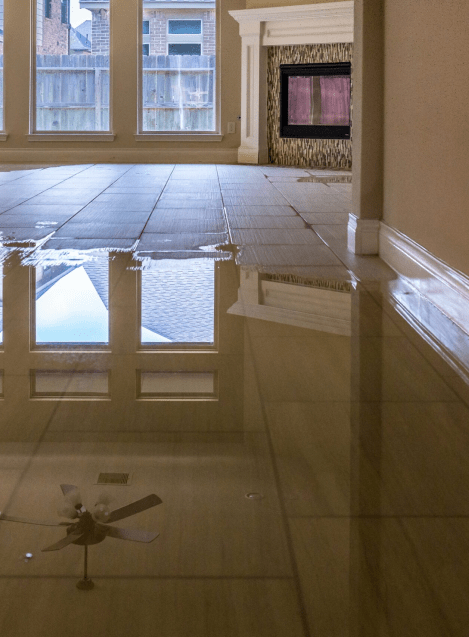

What is Considered Water Damage?

Water damage that occurs from sudden damage and some natural disasters are covered under home insurance policies. This would involve the following situations:

- Sudden and accidental leaks that occur in less than 2 weeks

- Burst pipes

- Washing machine leaks

- Refrigerator leaks

- Garbage disposal leaks

- Wind-driven rain (including hail storms, however, rain alone is typically not covered)

- Earthquakes (in some areas this is covered, but is typically sold as a separate policy)

- Slab leaks (State Farm is the only carrier that excludes slab leaks)

Flood Damage vs. Water Damage

Many homeowners commonly confuse flood damage with water damage, but it’s important to know that these are two very different things. Flood damage occurs when there is excessive water on land that would otherwise be considered dry. Water damage occurs before water touches the ground.

Water damage is almost always covered under a homeowners insurance policy, whereas flood damage is not covered under homeowners insurance.

Flood damage insurance should be purchased separately through either a private insurance group or the National Flood Insurance Program (NFIP).

The Following are not covered under homeowner’s Insurance:

Flood Damage: As mentioned above, flood damage is not covered under homeowners insurance and is not the same as water damage.

Gradual Damage: Some insurance policies will not cover issues that have been existing for a long period of time, typically longer than 14 days. For example, if you have a pipe burst as a result of old pipes that you did not replace, the insurance provider might find you at fault for neglecting to take care of your pipes and not covering the costs for damages.

Source of Damage: Most insurance policies do not cover the source of the damage - For example, if your home has water damage that was caused by a broken dishwasher, the costs of replacing the dishwasher would not be covered under the policy.

Did You Experience Water Damage? Follow These Steps

This is a major concern for many flood and water damage victims. Oftentimes when homeowners experience a flood or water damage, they can no longer live in their home while repairs are being done. Some living expenses might be covered under your insurance policy during that time where your home is uninhabitable. This can include things such as meals, laundry, transportation, and pet boarding.

In order to increase your likelihood of having your living expenses covered, you’ll want to:

1

Collect Evidence of Damaged Property

If you have experienced water damage, the first thing you want to do is collect evidence of any damaged property at your home. Photos and videos are the best way to document the damage. Make sure to also take photos/videos of the floor.

While it might be tempting to throw broken items away - avoid doing so. You’ll want to save any damaged items as evidence for your property damage claims, including filtration systems, pipes, garbage disposals, water heaters, washing machines, or any other devices.

2

Call a Licensed Plumber

A plumber’s incident report will end up serving as additional proof for your insurance claim. The report will provide a timeline of how long the leak occurred and where the leak came from. Insurance companies will not cover leaks that lasted longer than 14 days, which is why it’s critical for you to hire a plumber as soon as you notice any sign of water damage.

3

Contact a Licensed Public Adjuster

Water damage claims can be time-consuming and confusing if you’ve never filed one before. To make matters more difficult, insurance companies will often try to avoid paying for water damage. The first thing your insurance provider will do after you file a claim is a process known as “field scoping.” This involves them sending out a claims adjuster (who they’ve hired) to determine the exact cause of the damage and what they believe needs to be replaced.

The result is often you, the policyholder, being left with water damage that the insurance company does not want to reimburse you for in your claim.

A licensed public adjuster is on your side to help gather evidence that supports your claim and defend your claim against the insurance company to get you the payout you deserve.

What is the Difference Between a Public Adjuster and an Insurance Claims Adjuster?

Both public adjusters and insurance adjusters evaluate the damage done to your property. However, insurance adjusters represent the insurance company and therefore their focus is to benefit the insurance company.

Public adjusters work for you. A licensed independent adjuster can evaluate the damage to your home and help provide repairs, and assist with filing a claim with your insurance company.

Do You Need a Public Adjuster?

Licensed public adjusters can be extremely helpful if you have experienced water damage within your home. The below scenarios are two of the more common reasons why someone might hire a public adjuster:

- You disagree with your insurance claims adjusters’ evaluation of the water damage that was done.

- You are facing significant damage, potentially making the insurance claim difficult.

Experienced public insurance adjusters will help gather any data and proof that could help to restore your home and will work to defend your claim. But not just any public insurance adjuster will do - it’s important to choose a public adjuster who has years of experience in dealing with insurance companies. They will be able to effectively speak with the insurance company about your claim, simplify the claims process and ultimately get you the payout you need for repairs.

How Excel Adjusters Can Help With Your Water Damage Claim

At Excel Adjusters, our goal is to ensure your rights are upheld during the water damage process and maximize your payout. If you experience water damage, we will accompany the field insurance adjuster during the field scoping process and help you negotiate a fair payout.

We are not provided by the insurance company, making us fully independent and able to prioritize your needs as the policyholder.

We’ll help to:

Notify Your Insurance Provider

Whichever step of the claims process you are at, it helps tremendously to have a public adjuster speak with your insurance provider on your behalf. You might be wondering, why do I need a public adjuster when I can get my own repair estimates and talk with the insurance company myself? While it’s true that you can go through the claims process alone, dealing with water damage claims requires in-depth knowledge of insurance policies and home repair. It is almost like speaking a different language. Most homeowners have never filed a water damage claim before or spent any time understanding the intricacies of such claims. It’s also easy to become emotionally involved since your valuables and livelihood are at stake.

Maximize Your Payouts

As your licensed public adjuster, we know how to speak with insurance carriers about water damage claims and do everything in our power to get you the money you need.

Many contractors and floor experts are actually not licensed by the Department of Insurance and therefore are not legally allowed to represent you on your water damage public claim. But as your public adjuster, we are licensed by the state and can provide legal representation for you throughout the claims process, helping you to have one less thing to worry about.

Guide You Through the Water Damage Claim Process

We are there to support you during the entire claims process - this includes advising you and negotiating payouts with your insurance company. We also handle any necessary paperwork.

We only charge a small percentage based on what we settle for with your insurance. There are no upfront costs to you, making it affordable to get the help you need.

Assist with Every Stage of Your Water Damage or Flood Claim

Whether you’re at the beginning of filing a water or flood damage claim, or several weeks into the process, we can help.

- If your insurance company is refusing to cover ALE or Loss of Use expenses, we can work with your insurance company in an attempt to get you reimbursed for any living costs you incurred in your temporary home.

- Sometimes insurance companies will try to cut corners in your repairs by doing a poor repair job to your floors, hiring cheap damage rebuild companies, and failing to remove cabinets for drying when the drywall has been damaged. If you are not happy with the repair of your hardwood floors, we can help negotiate with your insurance company in order to get the “like-for-like” standard outlined in your policy. Also known as the “like kind and quality,” if your insurance policy includes these terms, you are entitled to receive a payout from your insurance company that covers the entire cost to replace items of the same quality as what you previously owned. Again, some insurance policies cover replacement costs, while others might not cover a replacement cost, so each situation is unique to your specific policy.

- If your water damage rebuild insurance claim has been denied, we can speak with your insurance company and provide evidence and reasoning as to why your water or flood damage claim should be covered by your carrier.